- Wealth Protection. Swiss Quality.

Inflation is the general increase in the price levels of an economic area over a certain period of time. The national consumer price index (CPI) is used to measure this in Switzerland and elsewhere. If this index rises, fewer goods or services can be bought with the same amount of money than before (e.g. 100 CHF). As a result, the purchasing power of money decreases with inflation.

This affects virtually everyone, but savers who leave their money in the bank are most affected.

Please use our inflation calculator and see how much you stand to lose through inflation. You can find out how you can protect your assets below.

Source: Federal Reserve Bank Of St. Louis, EOD Historical Data

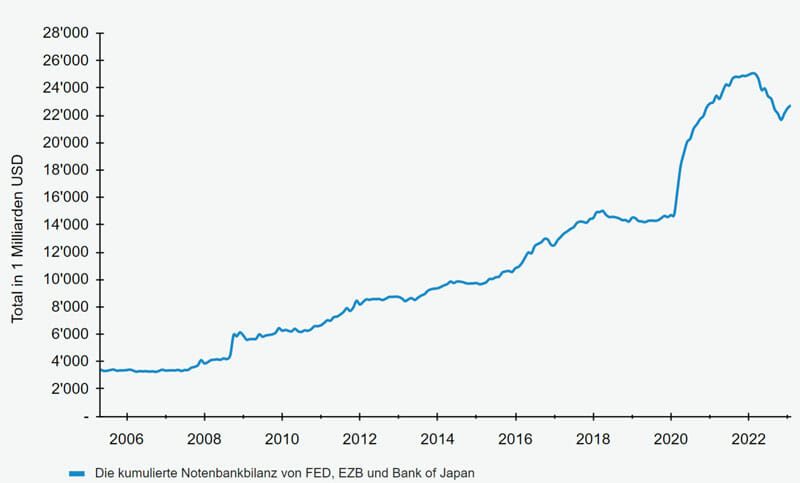

The equivalent value of a currency unit remains the same if money supply and economic growth move in lockstep. A faster increase in the money supply will sooner or later lead to inflation.

Central banks around the world have expanded the money supply extremely since the beginning of 2020 due to the Covid-19 pandemic. At the end of 2020, for example, there were around 25 percent more US dollars than at the beginning of the year. The more units of a national currency there are, the less each unit is worth. Purchasing power is diluted. At the same time, supply bottlenecks arose worldwide due to the Covid pandemic. Many goods became scarce and therefore more expensive, causing high costs and slowing economic growth. This created the perfect environment for the rapid rise in inflation in the US and Europe in 2021.

The most common measure is the annual percentage change in the consumer price index. The CPI measures inflation based on the price development of a basket of goods, which includes the most important consumer goods, rent, petrol and other essential household expenses.

The weighting of the basket of goods is updated annually. Prices for asset classes such as real estate, precious metals or stocks are not included in the basket. If these so-called asset prices were included in the calculation, we would have had a much higher inflation rate in recent years

The current basket of goods of the Federal Statistical Office can be viewed under National Consumer Price Index.

In an inflationary economic environment, saving in a bank account that does not generate interest is not worthwhile. On the contrary: Due to the rising prices of everyday goods, your savings are constantly losing purchasing power. Retirement savings that are held in a bank account are also affected. In the following short video, we explain why maintaining purchasing power is very important for your assets.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationUse our inflation calculator to see how much you are directly affected by inflation and how much your money loses purchasing power over time in a bank account.

The online calculator aims to show a hypothetical future course of the purchasing power deterioration of each currency. The value of money is assumed to be the purchasing power of money. The loss in value due to inflation therefore results from the loss of purchasing power of money over the period under consideration. On the basis of the parameters entered, the inflation calculator shows how the value of money is impacted over the selected period and states for each year the value of today’s purchasing power as well as the assumed future loss of value in relation to the beginning of that period.

The assumed future inflation rates and return expectations of the RealUnit may differ from the values actually recorded in the future. The results of the calculations are for information purposes only and do not constitute an offer or a solicitation of an offer. There is no guarantee for the currency, accuracy and completeness of the results. RealUnit Schweiz AG assumes no liability in connection with the calculation results. Investment decisions should be made after a thorough reading of the current prospectus, which can be found on the Downloads page.

First, think about how much money you will actually need in your account over the next few years to implement your plans. Also factor in unforeseen expenses, such as purchasing a replacement for a kitchen appliance. You should also consider the rule of thumb that you should have three months' household income available in your account at all times. You should let the rest of the money work for you and invest it.

Seek advice from your bank and draw up a personal risk profile. You should state your goals of capital preservation and inflation protection and also discuss your expected return on your investment. The basic rule for all investments applies here: the higher the expected return, the higher the risk. Conversely, this means that the higher your security expectations, the less your investments can fluctuate. The investor profile should be revised at least every 2 years based on your current life circumstances.

Most banks will recommend their own funds and investment vehicles. These have the advantage that your investment is spread across many different asset classes. The big disadvantage, however, is that for conservative investors these products mainly contain bonds with a allocation of between 45 - 70% of your total investment. These supposedly safe bonds lose value with every interest rate increase. Most investment professionals therefore advise against buying bonds in an inflationary environment, as it is very difficult to achieve a positive net return at all with debtors with good credit ratings.

The focus should be on scarce, real assets, as they can keep up with price increases.

The following are considered useful investments in this context:

- 145 kg physical gold

- 4,895 kg physical silver

- Focus on listed stocks mostly from Switzerland

- Healthy and solid companies with crisis-resistant business models and long-standing dividend policies

- Short-term liquidity in bank deposits

- CHF 4,500,000 in physical banknotes outside the banking system

- Unlisted stocks and alternative funds

- 18.6 Bitcoin (BTC)

- 100 Ether (ETH) staked

*stored outside the banking system in Switzerland

Balance as of 31.03.2026